Interac Corp. has only been around since the 1980s, but there is no denying the impact that it has had on Canada’s many markets and industries. As the creators of a variety of important payment services and systems, Interac has become the cornerstone of how many Canadian citizens make payments.

However, this variety of services and products also comes with a price – it can be hard to tell exactly which one suits your needs, especially if you are doing more than simply paying for something online. The more specific your requirements are, the harder it becomes to find the right service.

But what are the differences between major Interac products like Interac Online and Interac e-Transfer, and what are they meant for? Whether you have used an Interac product before or are brand new to this as a whole, it is important to understand what they actually are.

Interac Online vs Interac e-Transfer vs Interac Debit

The three most notable services that Interac offers are Interac Online, Interac e-Transfer, and Interac Debit. Each of these are services that see a lot of use within Canada’s financial sector, and are often used for a number of other purposes outside of official business uses.

However, at first glance, these might all seem like shorthand names for different ways of using the same payment system. While this is an understandable assumption, the three are actually significantly different, both for customers and businesses that are using them.

But before we get into any major comparisons, let’s go over exactly what all three services are and their intended uses.

What is Interac Online?

Interac Online is a payment method developed primarily for online shopping, allowing customers to pay directly from their bank rather than using an intermediary like a credit card. This effectively removes the need for a card when making online payments, at least in online stores that can support it.

This secure payment system works in real-time and with minimal hassle for either side of the transaction. The payment fees are competitive, with no hidden pricing increases or charges, and the authentication process does not cost any extra. Chargebacks are also blocked, and no private data is stored by Interac.

This has made Interac Online a popular choice for day-to-day online purchases, especially given that it has fraud monitoring and protection systems to prevent it from being used as a scamming tool. It is meant to be quick, easy, and convenient for both the sender and recipient.

Note that Interac Online is primarily meant for online shopping, and not for sending money from person to person. However, Interac does offer a similar tool that suits this purpose, which is Interac e-Transfer.

What is Interac e-Transfer?

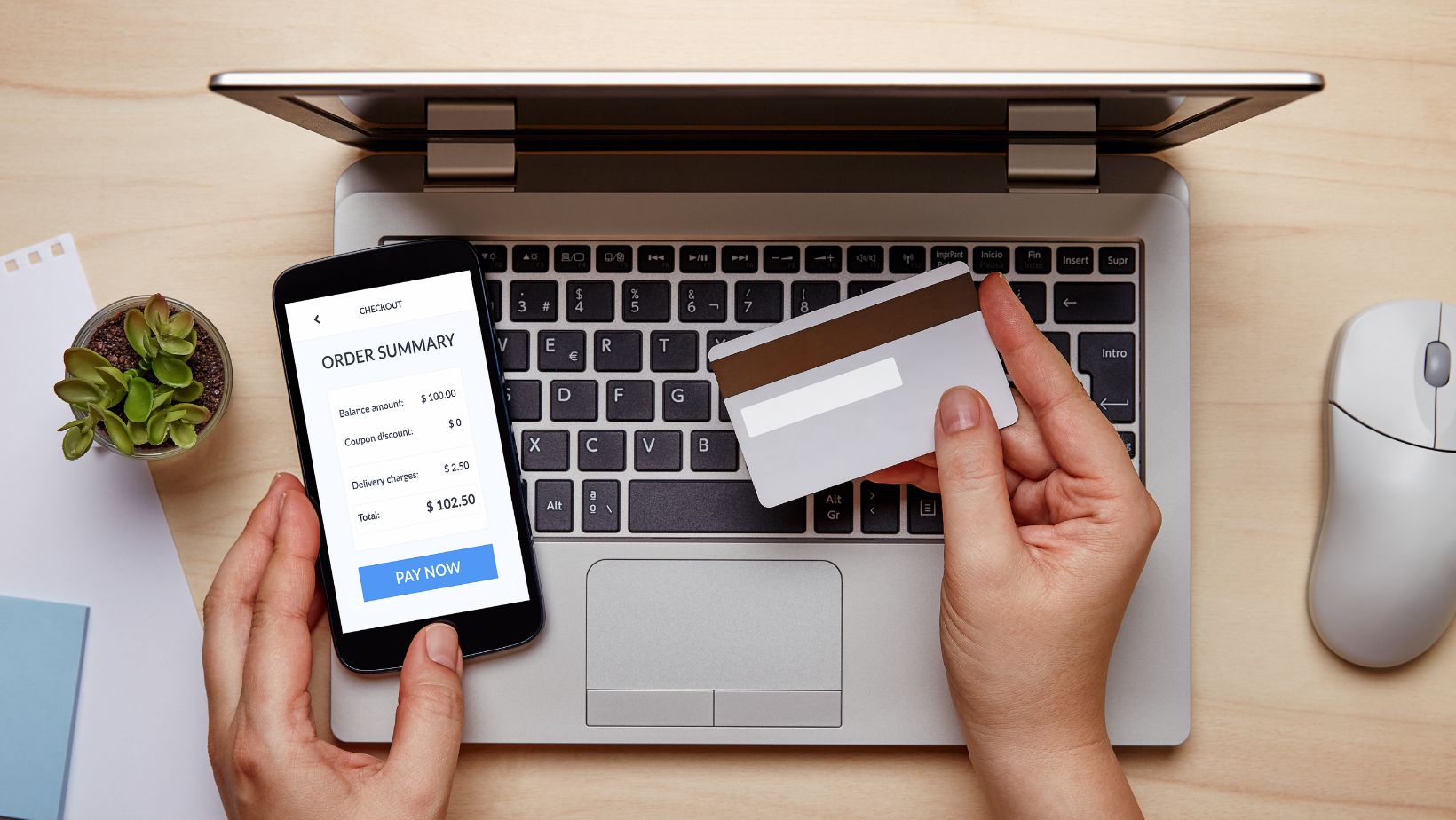

Interac e-Transfer is a system that enables transfers of money between both personal and business accounts using nothing but an email address or phone number. This makes the system highly flexible and convenient but also ensures proper security for both the sender and receiver.

Unlike a regular e-wallet system that serves as a literal wallet (allowing you to store money on the platform), Interac e-Transfer instead works as a middleman platform. Money is sent directly from the user’s online banking account, but without giving that banking information to the recipient. Interac e-Transfer Casinos are becoming increasingly popular due to these security features.

This makes the system far more secure since the only information that either side needs is the other person’s email address and/or phone number. The Interac online payment service obscures bank account information entirely but also still requires authentication from both sides of the payment before the money is sent.

Interac e-Transfer sees a lot of use as a day-to-day payment option, allowing for quick and easy payments with improved internet security. Not only that, but it is an incredibly fast payment method and has become a common choice for both personal and business banking in Canada.

What is Interac Debit?

Interac Debit is as simple as it sounds – a digital debit system that draws directly from your bank account, accepting a number of different existing debit card types. You simply connect a card to your account to draw directly from your bank, essentially giving your existing bank account some extra functionality.

In simple terms, Interac Debit is a practical way for merchants to accept payments from many different banks. It is Canada’s local debit network, so it is a common sight when making in-person purchases using your card.

While this might not be as groundbreaking as the other two services mentioned above, it is still a core part of how many businesses operate. In fact, if you want to use a debit card (not a credit card) in Canada, Interac Debit is often the mobile banking system you will use, whether you know it or not.

Interac Online vs Interac e-Transfer as a Customer

In this article, the big focus will be on Interac Online vs Interac e-Transfer. Interac Debit is important, but it is something you will be using anyway – the bigger question is whether Online or e-Transfer is more practical for your needs since they both serve the same role in distinctly different ways.

First, let’s look at both services from a customer’s perspective. Even if you are also a business owner, it can be important to understand how customers will use either platform, especially if you have just started your new business.

Interac Online As A Customer

Interac Online is designed primarily for easy online payments, keeping fees minimal. It debits funds directly from a user’s bank account and is often integrated directly into checkout processes as a selectable payment method for customers.

In other words, it is an alternative to paying with a card or through some other conventional payment option. You are paying for a product in the same way that a card would, with all of the usual data protection and seamlessness that you would expect from those services.

Interac Online serves as a reliable way to pay merchants quickly and easily since that is the entire reason it was designed. Naturally, this means that you are mostly going to encounter it when shopping online, but only when a site actually has it as an available payment option.

This is the main limitation behind Interac Online as a paying customer – it needs to be accepted at the site where you are trying to pay. While this is the same as any non-standard payment method, it also means that it might not be an option for every purchase, especially international ones.

Beyond that, Interac Online also is not really designed for non-commercial payments. While you could theoretically find ways to use it to transfer money to a friend, it is not the point of the service, and the fees included in each payment reflect that.

As a retail payment option, Interac Online is fantastic and even stands out more than certain longer-lived payment methods. However, it is also very limited to retail and shopping uses and is not usually going to be available for other reasons. You also can’t generally set it up yourself without having a business to connect it to.

Interac e-Transfer As A Customer

Interac e-Transfer is a money transfer system that focuses on moving money between bank accounts, regardless of whether they are business accounts or personal accounts. This is done through a specialized system that requires only an email address or phone number, meaning greater overall security.

When using Interac e-Transfer, you are essentially transferring money directly from one bank account to another using as little information as possible. This not only means more security but makes the transfers a lot faster than a typical middleman e-wallet could be.

One of the big advantages of Interac e-Transfer is its versatility. As a general-purpose transfer option, it can be used for both personal and business reasons, and is not tied down to being a specific kind of payment platform with strict rules and restrictions.

Interac e-Transfer has become a massive part of how many Canadians handle their payments, with billions of transactions occurring every year. This includes small businesses: there is a specific business version of e-Transfer that includes a payment confirmation system.

All e-Transfer payments need to be approved at either end of the transaction. Payments rely on the recipient sending the email address or phone number that is linked to their account, which the sender can then use to arrange the payment without any other information needing to change hands.

This makes Interac e-Transfer a very popular and flexible platform for a huge number of uses, including a lot of day-to-day money handling. However, it also is not a dedicated retail payment platform in the same way that Interac Online is, making it less practical for larger businesses with many more customers.

The other issue is that Interac e-Transfer requires some initial setup time and often has transfer limits that prevent extremely large transfers or purchases. You are also drawing money directly from your regular bank account, so its limitations and regulations still apply even if you are using e-Transfer as your payment method.

Interac Online vs Interac e-Transfer as a Business Owner

While the customer section was long, it is easier to understand these two platforms as a business owner. In simple terms, Interac Online is much more focused on actual retail payments and purchases, while Interac e-Transfer is more suited to moving money between two parties.

While Interac e-Transfer is great for smaller businesses as an alternative (or supplementary) option to normal payment methods, the specialized Interac e-Transfer for Business option is the best choice.

On the other hand, Interac Online is geared toward paying for products, which makes it a great way to accept customer payments. It does not require the customer to be actively using an Interac platform themselves, which can be more useful if you need to collect payments from a wider market.

In either case, the differences mostly come down to which one suits your business needs and the needs of your customers best. Both are compatible with mobile banking and common card types (such as VISA Debit Mastercard, etc.), but this depends on the bank, credit union, or lending bank the customer is using.

Either can be a great direct deposit option compared to other electronic services like e-wallets and can be used to both send and request money, depending on the situation. However, Interac Online is clearly focused on retail payments, while Interac e-Transfer is undeniably a primarily personal platform.

Interac Online vs Interac e-Transfer: The Pros and Cons

There has been a lot of detail in this article, so let’s break everything down into a simple pros and cons list. Remember: neither of these platforms is necessarily better than the other since it all depends heavily on what kinds of payments you will be making.

Interac Online Pros

- A fast and effective payment gateway that reduces delays for both the customer and the business.

- Simple structure that makes payments quick and painless.

- Fast transfer periods compared to some other payment processors.

- Improved security measures, including fraud scanning and protection that make sure that all payments are legitimate and processed as they should be.

- Low fees that lead to lower charges on even large incoming payments.

- No need to store private data, meaning reduced costs for the business and more privacy for the customer.

- Transparent pricing for business use.

- No authentication costs, meaning no extra costs are passed on to the business or customer.

- Effective fraud detection systems that can both identify and prevent fraud in a number of different contexts.

- Compatible with a wide range of banks and cards.

- Able to work across different banks (i.e. an account from one bank transferring to another).

Interac Online Cons

- Less practical for non-business uses and is not designed for handling personal money or quick transfers between friends.

- Only available for customers of certain banks, or for certain corporate bank accounts if you are using the business version.

- Not designed for a personal bank account, i.e., a savings account.

- There are no guaranteed refunds for customers due to the money being directly transferred into the seller’s account. However, sellers may choose to offer their own refund system.

- Occasional delays between accounts from different banks.

Interac e-Transfer Pros

- Incredibly fast transfer periods, often within 30 minutes or less.

- Improved security since you only need to give over a single piece of information to arrange a transaction.

- Better protection if your account is ever hijacked since Interac requires both parties to approve a transaction before it can be sent.

- Extremely convenient and easy to use, with barely any setup required.

- Easier, simpler payments that can be made almost anonymously if needed.

- Reduced or eliminated wait times for business payments.

- Bulk disbursement options under Interac e-Transfer for Business, making it easy to use for large-scale purchases.

- Simple invoicing systems that do not require a lot of customer information to be kept on file.

- Ability to set up auto-deposit/automatic funds transfer features.

Interac e-Transfer Cons

- Small (roughly $3000) transfer limits for non-business users, sometimes lower if the bank decides to reduce them even further.

- Only available for customers of certain banks or for certain corporate bank accounts if you are using the business version. For example, the National Bank allows it, but smaller lending services may not.

- Potential issues for foreign exchange use or payments abroad.

- No functionality as mobile wallets or e-wallets, meaning that you can’t store money on the platform.

- Requires security questions to use automatic funds transfers if the recipient does not have Interac e-Transfer set up themselves, which can also lead to more delays overall.

While both platforms are obviously very different from services such as Google Pay or using your own Visa debit card, they are just as flexible. They have been used for many different purposes, from non-profit organizations accepting donations to customers handling a range of personal loan types (vehicle loans, RRSP loan options, etc.).

Interac Online is clearly focused on business topics, and Interac e-Transfer is more of a general direct payment tool, but both can have their uses. Interac Corp. has great payment internet security features, and has become a major finance institution within Canada, so its products are inherently trustworthy.

If you are still unsure which one is right for your situation, look into them for yourself and see what Interac has to say about their products. There is no such thing as an all-purpose payment platform, and Interac has made sure to give each of their services some very distinct uses that fill a wide range of payment niches.